ManpowerGroup Inc. (NYSE: MAN)

ManpowerGroup Inc. (NYSE: MAN), a leading provider of employee placement and workforce services. As reported by beststocks.com, the company’s results are under pressure as governments and companies respond to the continued spread of COVID-19. While some employers are cautiously optimistic about the pace of economic recovery, Manpower has noted that many of the company’s clients may either delay the hiring of new workers, temporarily bar existing workers from coming to their place of business, or face long-lasting damage from changes in consumer behavior. We expect this disruption in the labor market to result in several quarters of disappointing earnings before Manpower returns to strength.

Recent Developments

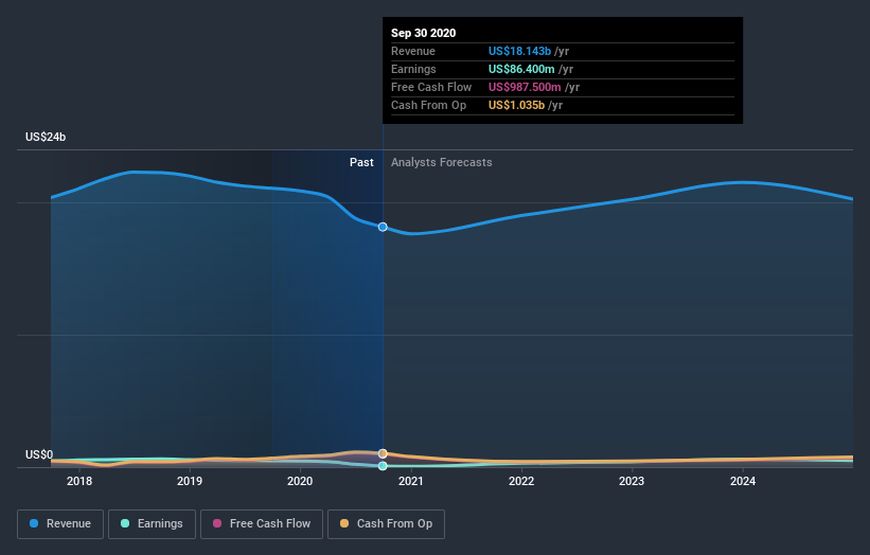

Manpower topped consensus-adjusted earnings expectations in the third quarter. On October 20, Manpower reported that adjusted EPS fell 39% in constant currency to $1.20 per share but topped the consensus of $0.62. Third-quarter revenue fell 15% year-over-year on a constant currency basis to $4.6 billion.

Although there is uncertainty from the pandemic, the guidance assumes no material lockdowns impacting economic activity in any of the company’s largest markets. The company expects 4Q20 adjusted EPS to be in the range of $1.06-$1.14, including a $0.03 positive impact from currency. The company expects revenue to decline 10%-12%.

Earnings & Growth Analysis

Manpower organizes its business primarily by geographic region. In 3Q20, the company generated 46% of consolidated revenue in Southern Europe, 21% in Northern Europe, 20% in the Americas, and 13% in APME.

In the Southern Europe segment, revenue fell 15% in constant currency, while the adjusted operating margin was down 90 basis points to 4%. France comprises 57% of the Southern Europe revenue, and was down 17% in constant currency. The company says that although revenue from France continues to recover, the rate of improvement in the revenue trend has slowed.

In the Northern Europe segment, revenue fell 22% in constant currency. In the UK, which is the largest market in Northern Europe, revenue fell 22% in constant currency. The adjusted operating margin narrowed 180 basis points to 0.2%. The company estimates the UK will show a slight improvement in the rate of revenue decline during the fourth quarter.

In the Americas segment, revenue fell 11% in constant currency. All countries included in the Americas segment experienced revenue declines. U.S. revenue declined 13%, Mexico declined 9%, Canada fell 10% and other countries within the Americas declined 6%. The adjusted operating margin narrowed 20 basis points to 5.2%. The company expects to see a revenue decline of 9%-11% in 4Q20.

Revenues in Australia declined 8% in constant currency. In Japan, revenue grew 5% on a constant currency basis in 3Q20. The company expects the Japan business to continue to perform well and anticipates fourth-quarter revenue to be flat or see low single-digit growth. The company expects revenue to be down 4%-6% in the fourth quarter for the APME segment.

At the expense line, the adjusted operating margin narrowed 100 basis points year-over-year to 2.6% in 3Q20. For 4Q20, the company expects the adjusted operating margin to be down 130 basis points, in the range of 2.3%-2.5%. Management intends to continue strong cost actions but at lower levels of year-over-year SG&A reductions as activity levels progressively increase.

Management & Risks

Jonas Prising is the chairman and CEO of ManpowerGroup. Mr. Prising became CEO in May 2014 after serving as president for a year and a half, and chairman in December 2015. He has worked for Manpower since 1999The CFO is John Thomas McGinnis. Mr. McGinnis has served in the role since February of 2016. Prior to ManpowerGroup, Mr. McGinnis worked for Morgan Stanley as Global Controller. Investors in the MAN shares face risks. The primary risk for MAN investors is the company’s sensitivity to global economic conditions and labor markets. With global markets slowing down due to the coronavirus, some of the company’s clients may restrict the hiring of new workers, temporarily bar workers from coming to their place of business, or lay off their existing workforce. Manpower also faces risks related to global trade, which could impact business conditions and employment in a range of industries. The company has a high exposure to Europe, and thus has currency risks related to both the pound and the euro. The company also faces potential disruption in the staffing industry from new entrants such as Uber.

Company Description

Operating in 80 countries, the company manages a range of brands, including Manpower, Expersis, and Talent Solutions.

Valuation

Given challenges from the pandemic, we do not expect MAN to achieve significant multiple expansion until market conditions improve. We would consider returning the stock to our BUY list on signs of greater resilience amid staffing market weakness and stronger margins and earnings.

Non-GAAP revenue came in $35 million above management’s guidance though $55 million below consensus.

Second-quarter non-GAAP revenue fell 29% from the prior year to $910 million. GAAP revenue fell 15% to $1.15 billion. Management noted year-over-year timing differences for certain releases, including FIFA 21, which was moved to 3Q21 this year from 2Q20 last year, and Madden NFL 21, which was launched later in the 2Q21 than in 2Q20.

Electronic ARTS INC

Non-GAAP operating income fell to $27 million from $335 million in 2Q20.

Earnings & Growth Analysis

Full-Game Download bookings were down 58%. Mobile bookings rose 4% in 2Q. Packaged goods revenue was down 70%.

Management launched its biggest franchise title, ‘FIFA 21,’ on October 9. This followed the launch of its second-biggest title, Madden NFL 21, in 2Q. EA Play is the company’s videogame subscription service bundle, in which the company sells access to a bundle of games for a monthly fee. So far, the company has done platform deals for EA Play with Valve/Steam and Google Stadia. It also recently signed a deal with Microsoft for EA Play to be offered on Xbox Game Pass in November, in conjunction with the new Xbox console launch. EA Play has 6.5 million subscribers.

Financial Strength

Outlooks are stable.

With its 2Q results, EA initiated a dividend for the first time in its 31-year history as a public company. We are setting an FY21 dividend estimate of $0.34, representing two payments in the second half of FY21, and an FY22 forecast of $0.70.

EA did not repurchases shares in 2Q, but did announce a new share repurchase program with its second-quarter results.

Management & Risks

As we predicted, investor sentiment regarding EA and other ‘stay-at-home’ stocks has dimmed recently on news of positive COVID vaccine trials.

Valuation

EA shares lost about 9% on news of a recent positive vaccine trial, which the market may be interpreting as a negative for so-called ‘stay-at-home’ stocks.